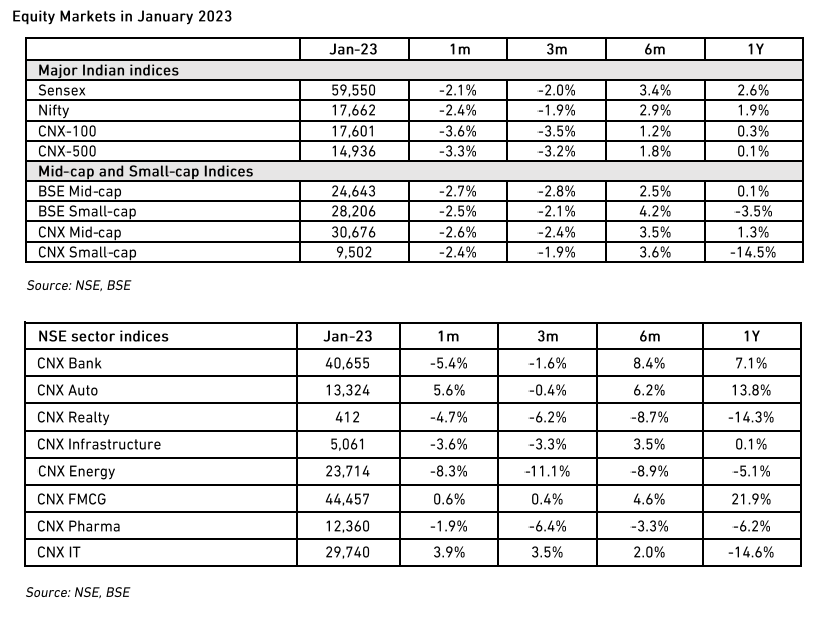

EQUITY MARKET OUTLOOK - 09 Feb 2023

The strong Union budget for FY24 is positive for the equity markets in the medium term. The fiscal prudence, combined with improved quality of expenditure, paves the way for a multi-year macro sweet spot - high GDP growth with stable financial conditions. In this context, we believe that growth stocks and quality will make a comeback in CY23, and the value rally is likely to fizzle out. The caveat is that valuations continue to matter and high PE stocks without support from earnings and cash flows may underperform. Also, we think the market will re-focus on quality metrics like strong balance sheets, return ratios and management strength.

Union Budget FY24

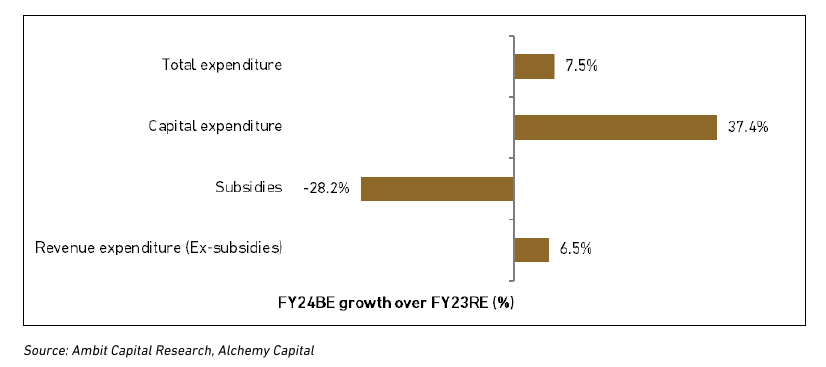

Capital Expenditure

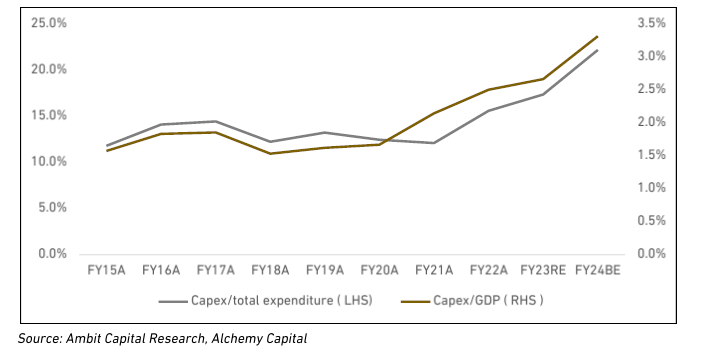

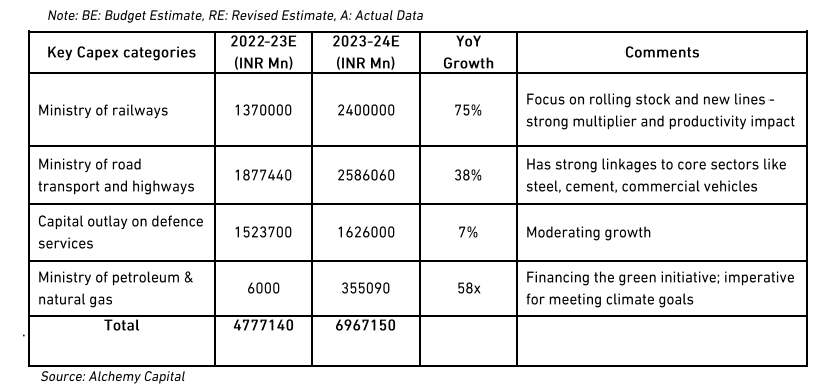

The standout feature was the surge in capital expenditure – raised by 37% to Rs 10tn. This was driven by increased allocation to railways, road construction and the green initiatives of the petroleum ministries. All these categories have significant multiplier effects on the economy and should help improve India’s long-term growth potential. This breaks the multi-year trend of India’s public spending shifting towards revenue expenditure (including subsidies).

Taxation

The other positive came from the direct tax proposals. Market fears of increased capital gains tax on equities proved unfounded – they were left untouched. In addition, there were marginal cuts in income tax rates across all income groups. In our view, the tax cuts are not material enough for a significant consumption boost, but we see them as a positive signal of the government’s approach to taxation.

Income Tax

There were marginal cuts in income tax rates across all income groups. The threshold for tax brackets was raised and the peak rate was cut to below 40%, which is a strong positive signal. The other important subtext is the strengthening of the new tax regime – we see clear signals that the government intends to fully transition to an exemption-free code over time.

Capital Gains Tax (CGT)

There were worries about a rationalisation of capital gains tax and a higher resultant incidence on equities. That was left untouched and, to that extent, a positive for the markets. We do not see the case for equating CGT across asset classes. The taxation of the underlying debt and equity are different and the CGT rates should reflect that difference, in our view.

Life Insurance

The new tax proposals are negative for life insurers in the medium term. At the bottom end, the transition to the new regime will reduce buyer incentives for the savings products, which are a large part of life insurers’ portfolios. At the top end, the capping of premiums at Rs 500k means that HNIs are now excluded from the market – as is the lifetime value of clients as upselling is capped beyond a point. This, we believe, would lead to a moderation of insurers’ rich valuations over time. We have been very selective about investing in this sector and will be even more cautious after this budget.

Fiscal deficit

Sticking to the Consolidation Path

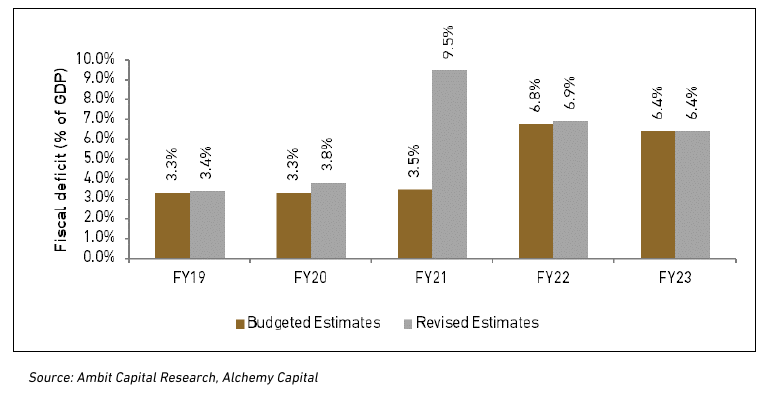

Despite these expansionary measures, the fiscal deficit contracted. A 50bps contraction to 5.9% in FY24 reaffirms the government’s commitment to bring the fiscal below 4.5% by FY26. India had taken up the fiscal deficit targets in the wake of Covid and this is a good time to start to consolidate. A reduction in the fiscal deficit does constrain growth – but we think that the changing composition of spending towards capex cushions the impact. The flipside is that the conservative fiscal policy should help the overall financial stability and keep long bond yields in check.

Reasonable Assumptions

This has been achieved with moderate assumptions on tax collections. GDP growth assumptions are at a moderate 10.5% and tax collections are largely in line with that at 11.5%. These are reasonable buoyancy assumptions and we see very little risk of a shortfall. Interestingly, the tax collections for FY23 overshot the budget estimates – a rare occurrence in India’s history.

Key Risk: Global Macro

Global macro is an imponderable here. The fiscal maths has been built on a sharp cut in food and fuel subsidies. This is reasonable – there was a one-off spike in FY23 due to global oil and commodity price inflation. If this assumption goes awry, however, the government may have less room to maneuver and may need to cut back on the planned capital expenditure to keep the fiscal in check. We shall be monitoring this trend closely.

Markets – Stick to Quality

Supportive Macro

Our constructive view on the markets is underpinned by an expectation of a robust macro. Sure, there are near-term growth challenges from a high base effect, slowing global growth, and the withdrawal of excess liquidity. Over the medium term, however, we believe multiple tailwinds will propel growth to a sustained, multi-year, 6%+ range.

-

Consumption should recover as incomes continue to rise and inflation moderates from the post-pandemic supply shock.

-

The capex cycle should recover, helped by both public and private spending. We have already seen anecdotal evidence of this in the order books of capital goods manufacturers and the budget outlay adds further momentum to that trend.

-

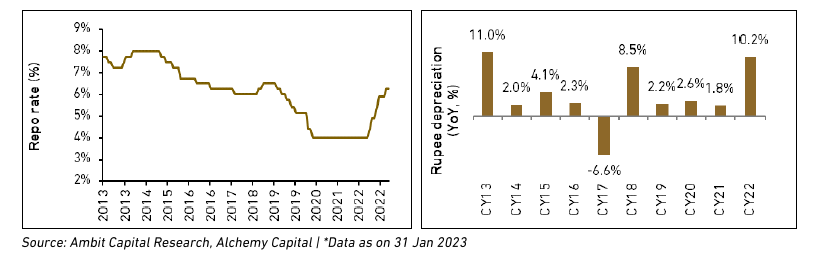

We see an extended period of financial stability with interest rates topping out at levels that are in the mid-range of the historic range. Moreover, the currency weakness seems to be orderly and is unlikely to cause a major shock. This is helped, of course, by both corporate and consumer balance sheets being largely healthy following the deleveraging of the last 3-4 years.

Key Mantra: Growth

We continue to focus on high-growth companies as our core investment thesis. The value rally of 2022 may not sustain into 2023, in our view – the re-rating seems to be over and it is difficult to find pockets of egregious undervaluation at this stage. On the other hand, the strong economic cycle is throwing up a broader set of high-growth companies to choose from, with strong balance sheets and high profitability ratios.

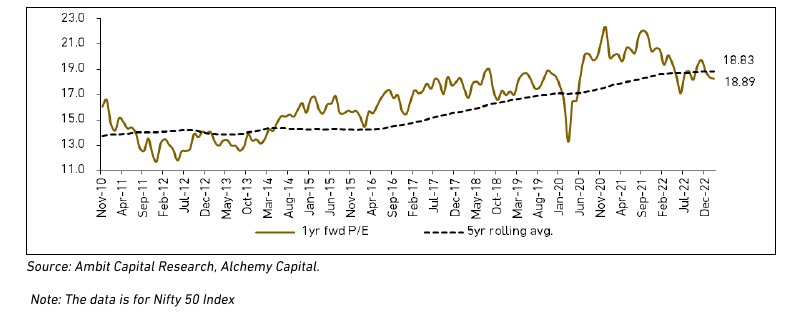

Tread Carefully on Valuations

The extended valuations on the broader market, however, make stock-picking more difficult. 2022 was brutal for companies with rich valuations, and many winners from the 2011-2020 decade have been consistent underperformers in the recent past. We continue to use valuation as a filter for high-growth companies and are careful of overpaying. We are not, however, averse to buying high P/E companies as long as growth and cash flows support these valuations.

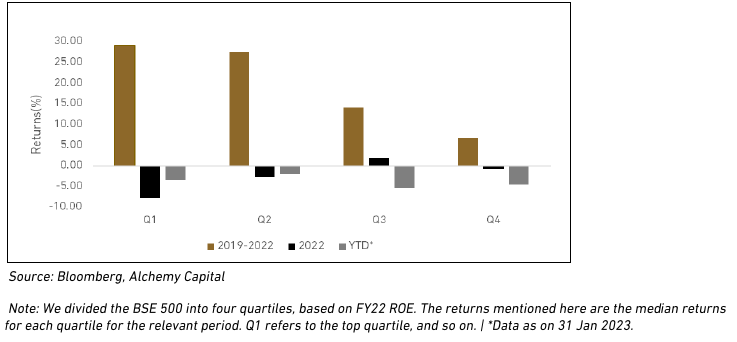

Stick to quality

High-quality companies were laggards in the value rally of 2022. Filters like strong balance sheets, quality management/business models, and robust return ratios did not seem to work last year. We see the tide already turning in 2023 and see quality making a comeback in CY23. We are sharpening our quality filters for our stock-picking and have exited exposures where we see challenges on the business or management front.

Adani Impact

Final word: We do not see the sell-off in the Adani group stocks triggering a broader contagion in the market. We had stayed away from this group due to our filters on leverage. We also, at this stage, do not see this triggering any sort of crisis in the financial system, as bank exposures are limited to ~1% of net advances, going by the disclosures made so far.

Source: Alchemy Group Research, Bloomberg

Disclaimers

Information and opinions contained in the document are disseminated for the information of authorized recipients only and are not to be relied upon as advisory or authoritative or take in substitution for the exercise of due diligence and judgment by any recipient. This document and its contents has not been approved or sanctioned by any government authority or regulator.

This document does not constitute an offer to sell or a solicitation of an offer to buy any securities. Any such offer or solicitation will be made only by means of the appropriate confidential Offer Documents that will be furnished to prospective investors. Before making an investment decision, investors are advised to review the confidential Offer Documents carefully and consult with their tax, financial and legal advisors. This document contains depiction of the activities of Alchemy and the investment management services that it provides. This depiction does not purport to be complete and is qualified in its entirety by the more detailed discussion contained in the confidential Offer Documents. Any reproduction or distribution of this document, as a whole or in part, or the disclosure of the contents hereof, without the prior written consent of Alchemy, is prohibited.

Performance estimates contained herein are without benefit of audit and subject to revision. Past performance does not guarantee future results. Future returns will likely vary, and investment results will fluctuate. In considering any performance data contained herein, prospective investors should bear in mind that past performance is not indicative of future results, and there can be no assurance that the Fund will achieve comparable results or that the Fund will be able to implement their investment strategy or achieve their investment objectives will achieve comparable results.

The information and opinions contained in this document may contain “forward- looking statements”, which can be identified by the use of forward-looking terminology such as “may”, “will”, “seek”, “should”, “expect”, “anticipate”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof. or other variations thereon or comparable terminology. Due to various risks and uncertainties, including those set forth under the Private Placement Memorandum/ Investment Agreement actual events or results or the actual performance of the Fund may differ materially from those reflected or contemplated in such forward-looking statements.

These materials discuss general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Certain information contained in these materials has been obtained from published and non-published sources prepared by third parties, which, in certain cases, have not been updated through the date hereof. While such information is believed to be reliable, Alchemy does not assume any responsibility for the accuracy or completeness of such information. Except as otherwise indicated herein, the information, opinions and estimates provided in this presentation are based on matters and information as they exist as of the date these materials have been prepared and not as of any future date, and will not be updated or otherwise revised to reflect information that is subsequently discovered or available, or for changes in circumstances occurring after the date hereof. Alchemy’s opinions and estimates constitute Alchemy’s judgment and should be regarded as indicative, preliminary and for illustrative purposes only

Performance results shown for the Fund are presented on a net basis, reflecting the deduction of, among other things: management fees, brokerage commissions, administrative expenses, and accrued performance allocation or incentive fees, if any. Net performance includes the reinvestment of all dividends, interest, and capital gains.

The net monthly return is derived by reducing the Fund’s gross performance by the application of the management fee, charged monthly in arrears, a subscription fee and a performance fee. The performance fee is charged annually and subject to a high water mark. Performance results are estimates until completion of the annual audit. Because some investors may have different fee arrangements and depending on the timing of a specific investment, net performance for an individual investor may vary from the net performance as stated herein.

Index performance and yield data are shown for illustrative purposes only and have limitations when used for comparison or for other purposes due to, among other matters, volatility, creditor other factors (such as number and types of securities) An index does not account for the fees and expenses generally associated with investable products. The S&P BSE 500 index is designed to be a broad representation of the Indian market covering all major industries in the Indian economy. The index consists of 500 constituents listed at BSE ltd. It is calculated using a float adjusted , market cap weighted methodology. The Rebalancing of the index occurs semi-annually in June and December.

7x5pjg85n7|00004A29|AlchemyIM|ThoughtLeadership|Description

7x5pjg85n8|00004A29B796|AlchemyIM|ThoughtLeadership|Description|1C71B778-9D02-4503-8A4D-A5DC71BC112B

ear47mtete|0000025CE9F8|ThoughtLeadership|Description|EC59EE21-9372-4FF3-B493-83A630BCD166